Apartment Completions Set to Peak in 2017, but Opportunity Remains Plentiful: Webcast Recap

MPF Research’s latest interactive webcast explored emerging construction narratives and ranked top markets for development viability. RealPage Chief Economist Greg Willett, MPF Research Vice President Jay Parsons and new RealPage family member Jay Denton of Axiometrics hosted the event.

A layered analysis of building volumes fueled the discussion. Parsons emphasized every aspect of the industry’s conversation around development pointed to one question: Is ongoing apartment construction finally peaking?

Supply and Starts

About 290,000 units completed in the core 100 U.S. metros in 2016, but deliveries “will soar in the coming months,” Parsons said. “Our current expectation is supply will peak in the second half of this year, with about 367,000 units completing on a trailing 12-month basis. That’s a 27% increase.”

What happens after 2017? “There’s a clear signal that new supply will taper in 2018 and 2019, when you look at the recent construction starts data,” Willett said.

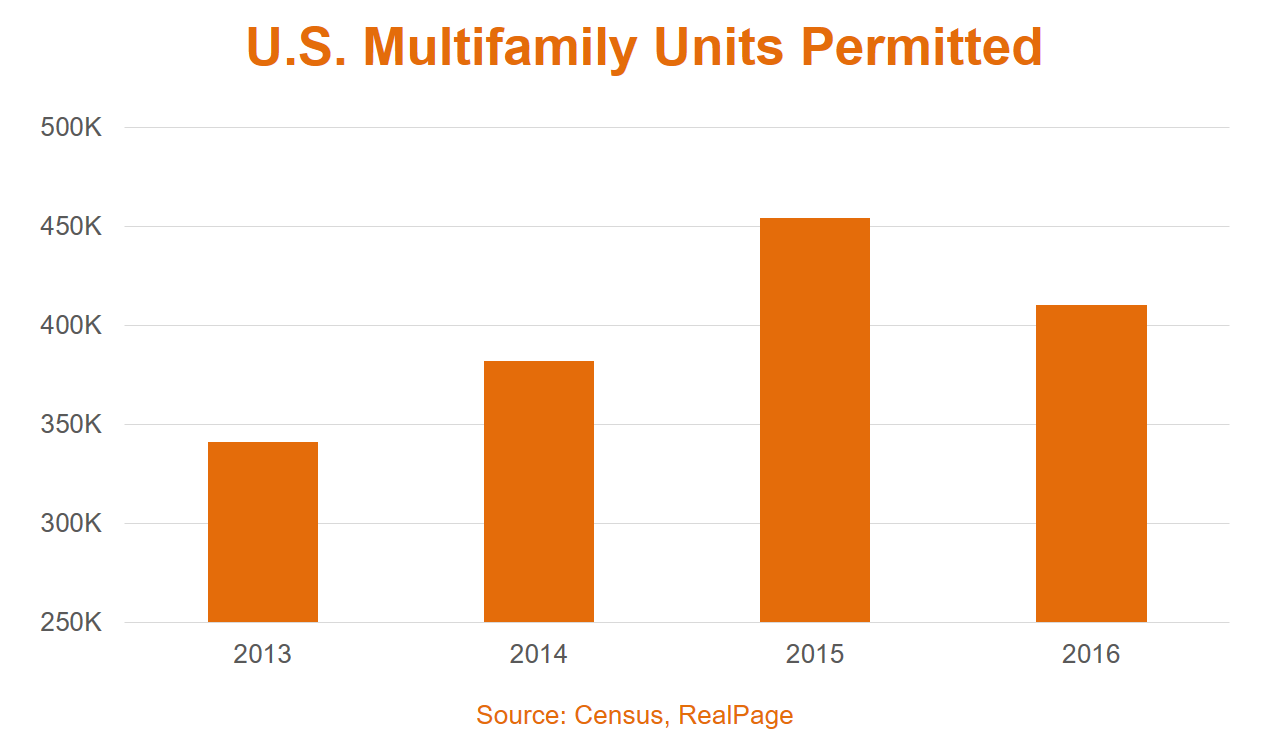

Denton said that the potential slowdown is even more pronounced in multifamily permit data.

“Nationally, we permitted just under 411,000 multifamily units in 2016 compared to almost 455,000 in 2015,” Denton said. “Holding above 400,000 still puts us well above the long-term norms, but I would agree that we are more than likely past the peak for new starts and permits.”

Data from RealPage partner Real Capital Analytics® (RCA) supports a downward trend. RCA reports a deep decline in land sales between 2015 and 2016. Parsons explained development sites are pricier and construction financing is increasingly difficult to secure.

“And related to that … the Fed’s survey of senior loan officers shows that banks are seeing declines in demand for construction loans and for multifamily loans more broadly,” Parsons said. “At the same time, they’re also reporting tightening underwriting standards.”

For now, completions remain the focal metric for performance. Denton noted supply is weighing on the market, especially as employment momentum slows.

“The good news? In most cases, I think 2017 will be a soft landing, and we’ll see performance accelerate again in 2018,” Denton said.

Suburban vs. Urban

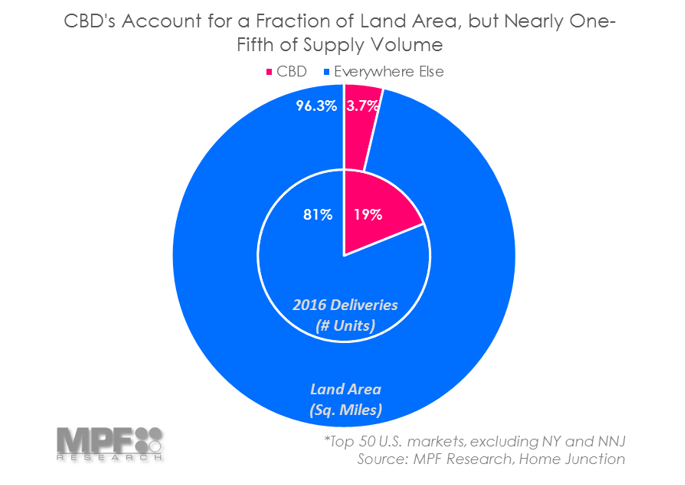

For those wanting to deploy capital, Parsons noted that top-tier suburbs in growth markets remain an attractive option.

“For the last decade, investors and developers have aggressively targeted construction in the urban core over the suburbs. In fact, in 2017, central business districts will see supply grow at a rate three times that of the suburbs nationally,” Parsons said.

The high barriers to entry, he explained, have shifted to high-end suburbs – those within close reach of jobs, transportation, retail, good incomes and high home prices.

“In those types of spots, developers run into issues finding sites due to NIMBYism and restrictive zoning. But if you can get deals done, you’ll see the benefits,” Parsons said. “We did an extensive analysis concluding that risk-adjusted returns are better in top-tier suburbs than what you’d get in the urban core – not just in this cycle, but over multiple cycles. And that performance gap has only widened in this cycle.”

Late-Recovery Economies

Late-recovery economies are also making a play. A few of the nation’s metros that have been slow to recover from recession, Willett said, appear to have some runway left.

“They aren’t adding new supply at historical norms, even though there’s now sound job growth at the same time the existing apartment stock has filled up, and that rent inflation is super strong,” Willett said. “I’d put the Inland Empire at the head of the list in that category. Sacramento and Las Vegas too, though it’s important to keep in mind how quickly activity can accelerate in Vegas.”

Denton threw San Jose into the mix.

“We show it as one of the few markets that has negative rent growth right now, and that tends to make people shy away. But you shouldn’t just look at today’s performance when considering what needs to be delivered two or three years from now,” Denton said. “Of course, it’s not like you can snap your fingers and start on a deal tomorrow. It takes time to get the pipeline restarted there, which is even more reason to look at this market.”

Denton and Willett both supported a case for Houston’s inclusion.

“Some of the big-picture questions we’ve had about Houston’s energy-influenced economic outlook feel like they’ve been answered recently – and they’ve been answered in a pretty positive way,” Willett said, adding oil prices appear reasonably stable and active rig counts are increasing. “You’ve got to get the neighborhood and product right, but I vote that it’s time to remove the red line from Houston.”

Some tertiary markets also show potential, though Parsons noted many such markets are already registering big construction numbers.

“From what’s left, Grand Rapids, Michigan and Greenville, South Carolina have been two of the strongest smaller markets in this cycle,” he said. “Neither have been ignored by developers by any means, but [both markets] likely could support more apartments due to healthy demand drivers.

“Then there are always the smaller cities around the California Bay Area – places like Santa Rosa and Santa Cruz,” Parsons said.

Redirecting focus to larger metros, Willett said regional players are likely to have success in some of the slower-demand markets that institutions generally will not consider.

“Let’s put most of the Rust Belt in that category,” Willett said. “There’s a strategy of targeting good neighborhoods that haven’t seen construction in 20 to 30 years, and going in to build moderately-sized properties of maybe 200 units. It’s an appealing, well-defined niche. But you do have to consider that it’s a shallow play in any given market.”

The interactive event also included insightful discussion on student housing, the recent marriage of MPF Research and Axiometrics and a comprehensive audience Q&A session.