What Does the Construction Date Reveal about the Apartment Stock?

Real estate investors are obsessed with numbers – recent sales, price per unit, cap rates, lease comps – the list goes on. But the obsession goes beyond the numbers. By trying to accurately predict the future, investors look at each data point as an opportunity to read between the lines to gain insight and an edge. This piece examines the concentration of multifamily product by year of construction across U.S. metros. Will the results prove that with time comes perfection, like a perfectly aged bottle of scotch, or is there growing evidence newer assets are the way to go?

To begin, MPF Research grouped our surveyed properties into two broad categories:

- Units built since 1990 (1990+)

- Units built prior to 1990 (Pre-1990)

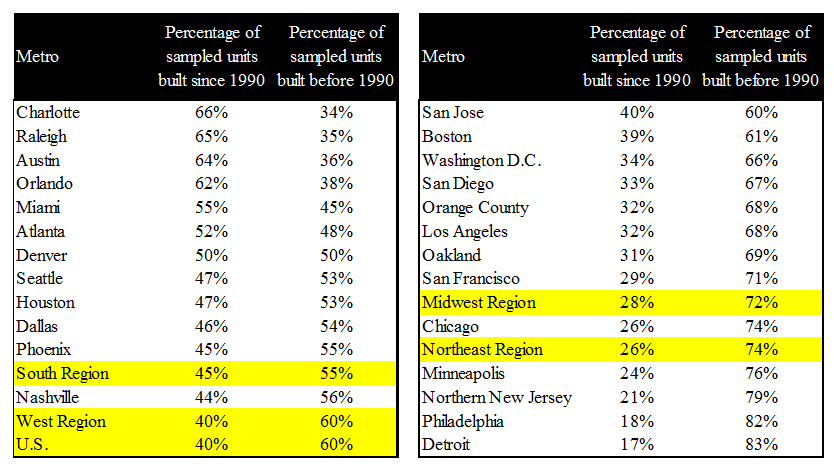

Regionally and by metro, the results are not surprising. Southern metros, which benefit from larger amounts of available land, population growth and employment growth, maintain a significantly higher concentration of newer properties. But what does this tell us and what are the implications for real estate strategy?

Specifically, the data has implications in four areas:

Specifically, the data has implications in four areas:

- Barriers to entry

- Underlying demand for newer product

- Development opportunities

- Investment strategies

With regard to barriers to entry, metros with a larger concentration of newer product are generally classified as high-demand, high-growth areas with younger populations and lower barriers to entry. Recently, MPF Research published a 10-part series on the busiest submarkets for development activity, and the results support this assertion. Four of the top 10 submarkets were located in Texas, two in Nashville and two in Charlotte. On the other hand, metros with a larger concentration of older units (built before 1990) generally maintain higher barriers to entry through some combination of limited land availability, strenuous zoning regulations or high land prices, all of which make projects economically less feasible. Furthermore, these metros tend to have more mature economies and older populations.

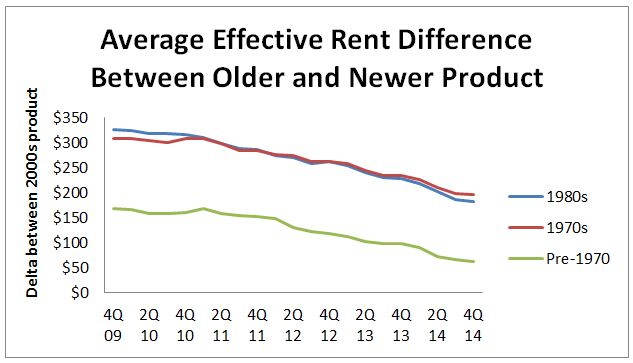

Demand for more expensive, newer product should be viewed in terms of short-term and long-term themes in the multifamily sector. On a short-term basis, an improving employment picture is boosting demand for apartment units which is benefitting all product age niches. Case in point, revenue growth at the national level re-accelerated in 2014, as vacancies remained low despite rising completion volumes. However, as the average effective rents between older and newer product converge, renters will eventually trade up to newer units with better locations and amenities. Furthermore, from a long-term standpoint, Millennial lifestyle choices, including the delay of marriage and kids and buying the first home, combined with Baby Boomers looking to downsize has increased the number of renters by choice, who have a tendency to rent newer, higher-end product.

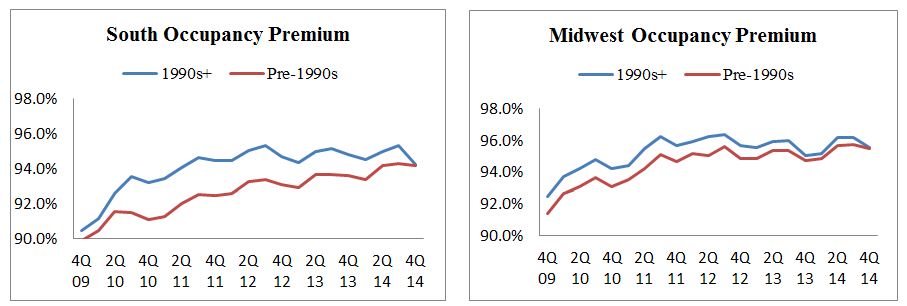

Given healthy levels of underlying demand for newer properties, how should we think about development opportunities today? This dataset combined with metro-level fundamentals, current and expected construction volumes, employment and demographic trends and costs of homeownership is helpful to determine where opportunities lie. For example, in a mature market like Philadelphia, Northern New Jersey, Minneapolis or Chicago, a lack of new product may represent a terrific development opportunity to capitalize on an underserved market segment. Conversely, if development opportunities are not warranted due to construction costs or economic or demographic headwinds, these same metros may be well-primed for redevelopment or value-add strategies. On the other hand, if you are looking to build in a high-growth metro, how do you differentiate your community (cost advantage or differential advantage) among so much competition? In the South region, the historical occupancy premium in 1990+ units suggests product differentiation through location, close proximity to transit, amenities, and resident service is the way to go. This theme appears true – although to a lesser extent – in the Midwest region. However, more recently, the occupancy premium for newer product is eroding as newly completed projects enter the lease-up phase. This trend represents a near-term headwind for the top end of the market.

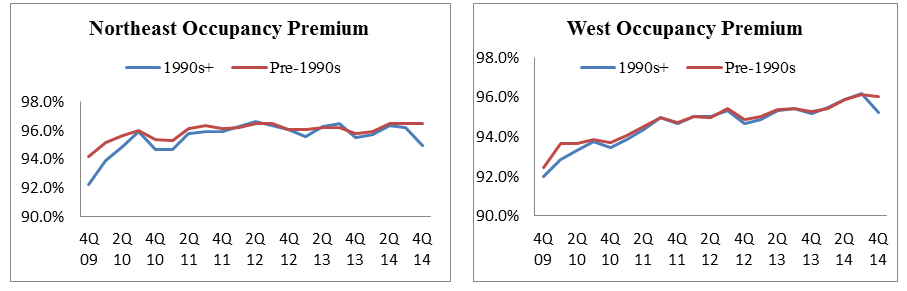

For comparison, in the higher priced coastal regions, newer product historically has not enjoyed the same occupancy premium. Furthermore, as affordability becomes a growing concern, demand has shifted to older, more affordable product. This suggests newer product must compete through a combination of price and attributes more so than in the South and Midwest.

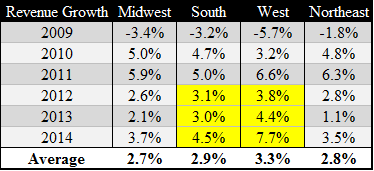

Turning to investment strategies, in the blog “Decomposing Apartment Returns and Strategic Implications,” we pointed out that this part of the cycle favors income returns over appreciation. As a result, we suggested core investors should focus on newer vintage assets that require lower capital expenditures as a strategy to enhance cash flows. Furthermore, future revenue growth is expected to favor those metros with wage growth necessary to absorb higher rents, lower homeownership rates, population growth and strong employment growth relative to supply expansion. To that point, revenue growth, which drives income returns, has been higher in the West and South for three consecutive years. Moving forward, MPF Research expects a similar trend over the next three years.

In conclusion, investors should use this period of strength in the multifamily industry to position their portfolio to take advantage of the underlying themes. This includes identifying development opportunities to capitalize on an underserved or growing market segment, seeking value-add opportunities inside the older stock of units within favorable metros and disposing of older assets, particularly those with incurable functional or economic obsolescence. By doing this today, you create a balance between growth and income objectives and produce an overall portfolio that will be better insulated against value loss during either a rising cap rates environment or an economic downturn.

(Image Source: Shutterstock)