Early Leasing Points to Continued Moderation in Student Housing

With the 2018-19 leasing season underway, results so far indicate another year of flat performance. New supply of purpose-built student housing remains at moderate levels for the fourth consecutive year, and performance is on pace with last fall.

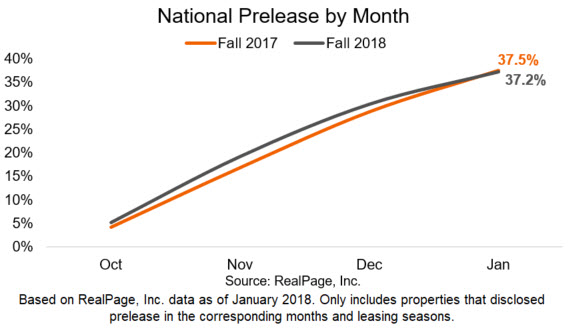

In 2017, the year-over-year spread in leasing velocity began to narrow around January and remained in line with the 2016 velocity throughout most of the year. Ultimately, Fall 2017’s leasing velocity fell slightly below the Fall 2016 average by August.

A similar trend is seen a few months into the 2018 leasing season. Prelease averaged 5.3% in October 2017, 103 basis points higher than in October 2016. In November and December 2017, leasing velocity remained ahead of previous years, but the spread tightened in January 2018. Leasing velocity averaged 37.2% in January, only 28 basis points below the prior year.

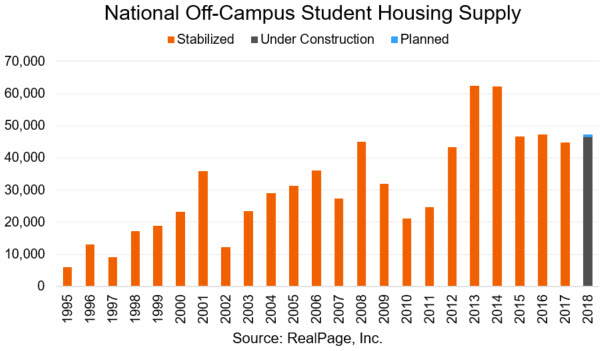

These results were anticipated given supply trends. A total of 46,000 new off-campus student housing beds are scheduled to be delivered for the Fall 2018 semester, with 900 beds still considered planned (though they are unlikely to be ready this fall). These figures are in line with the volume of new supply seen since 2015, though certain universities have seen fluctuations and even elevated levels of new supply.

There are several large markets recovering from elevated supply volumes in 2017, and some markets are expected to see performance moderate or even decelerate as supply increases this year.

Looking at individual assets, properties located closer to campus continue to see stronger results. On average, properties located less than a half-mile from campus were 41.1% preleased in January, up 61 basis points from January 2017. These properties were also averaging above $700 per bed for Fall 2018, with annual effective rent growth of 1.6%. This is in line with the current national average but below historical levels.

Properties located between a half-mile and one mile from campus were 34.6% preleased in January, up 89 basis points from last year. These properties are seeing the largest year-over-year increase in leasing velocity and the highest rent growth of 2.0%. And while they have continue to see the highest rent growth over the past few years, the average price per bed is only averaging $17 more than properties located more than one mile from campus.

And as traditionally seen, those located more than one mile from campus saw the lowest average prelease of 28.5%, which is a decline of 350 basis points from January 2017.