Apartment Completions Up, Rent Growth Down in 2017 Forecast: MPF Research Webcast Recap

MPF Research’s latest interactive webcast looked to 2017, exploring the outlooks for apartment fundamentals and capital markets. The live event was hosted by RealPage Chief Economist Greg Willett and MPF Research Vice President Jay Parsons and featured special guest Philip Martin of Chicago-based Waterton.

The initial discussion unfolded around the presidential election, a topic of particular interest among multifamily investors, owners and operators. Marking President-elect Trump’s win a surprising development that carries uncertainties, Willett noted there is some consensus on select broad moves the new administration could bring.

“We’ll probably get some tax cuts on the corporate level, and for individual households, too,” Willett said. “There should be a push for some deregulation in the financial sector. Trade policies seem likely to become more restrictive.”

Parsons added to the list increased infrastructure spending, another Trump agenda item.

“Most economists, regardless of political affiliation, really like that one, but you’ve got to question whether fiscal conservatives in Congress are going to go for the big bump in spending,” Parsons said.

Delivery Trends

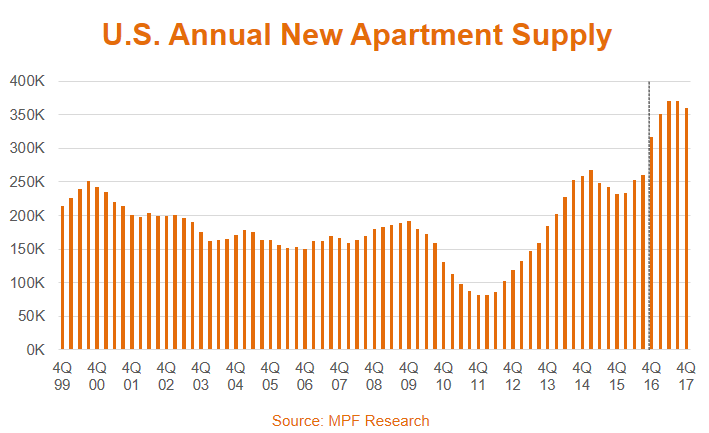

More predictable is the volume of apartment construction. Though multifamily permit volumes signal a slowdown in starts on the horizon and developers report that financers are increasingly hesitant to lend, multifamily development levels currently remain well above historical norms. MPF Research’s under-construction tally in the nation’s 100 largest markets totaled an impressive 561,000 units at the end of 3rd quarter 2016.

In terms of completed units, “we’ll flirt with 300,000 units or so of new supply in 2016,” Parsons said. “That’s the most we’ve seen in this country since the mid-1980s.”

Delivery volumes will continue breaking records over the next year, Willett said.

“This year we hit a three-decade high for new supply, and then we go up another 10% to 20% in 2017,” he said. “That alone tells everybody where the rest of this conversation is going.”

Apartment demand is expected to remain strong, but not at the same level of new supply. In turn, occupancy will likely decline. Occupancy around 96.1% is expected at year-end 2016.

“We’re then calling for a drop of 70 basis points in 2017, taking the figure to 95.4% or so,” Willett said.

Rent Growth Remains Solid

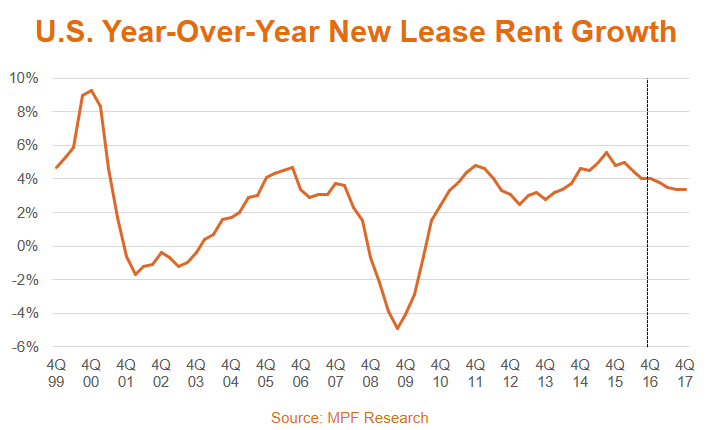

An analysis of pricing power capped the conversation of market fundamentals. Parsons outlined future figures.

“We expect annual growth in pricing for new resident leases to come in between 3% and 3.5% during calendar 2017, compared to the pace of 4% seen as of 3rd quarter 2016,” Parsons said. Those are “still very good numbers by historical measures, but lower than what we’ve seen for most of this cycle.”

Several key metros have seen softening recently. In some of those metros, operator sentiment appears to be the culprit, Willet explained.

“We’re seeing what we view as over-reaction to slight cooling of market fundamentals in some areas,” Willett said.

Parsons pointed to New York City and the Bay Area’s San Francisco and San Jose as examples.

“Our base-case assumption is that operators will pretty quickly realize that these markets remain healthy and will begin to push rents again,” Parsons detailed. “We’re forecasting 2017 rent growth of roughly 5% to 6% in the three Bay Area metros, and around 3.5% in New York.”

Still, market conditions appear to be driving weak performances in other metros – particularly those in which the local economy is dependent on the energy sector. Those struggles are expected to continue into 2017.

“Basically flat rents are forecast for Houston, and that expectation might be a little optimistic given that we’re calling for occupancy to drop quite a bit,” Willett said. “Expected rent growth also is weak, in part, because of energy sector exposure in Oklahoma City, Tulsa, Corpus Christi and Pittsburgh.”

Capital Markets and Deregulation

Shifting gears, Parsons and Willett examined capital markets.

“We’re on track to end 2016 with apartment sales volumes on par with 2015 levels,” Willett said. “Last year, our partners at Real Capital Analytics recorded $153 billion in apartment sales, and year-to-date through October, RCA shows sales volumes basically in step with the 2015 pace.”

The approaching year could prove more voluminous, with the incoming Trump administration likely to pursue deregulation.

“They will almost certainly target two of the hot-button regulations that commercial real estate buyers and lenders have complained about loudly: … the risk retention rules that have been blamed for slowing CMBS lending, and … the new rules on so-called High Volatility Commercial Real Estate loans, which are being blamed for slowing construction lending,” Parsons said.

Changes, however, would require time to transpire. Parsons, noting buyers and lenders could benefit from waiting out such changes, weighed immediate effects.

“I do wonder if we don’t see at least a little slowing in sales activity through the early part of 2017 to allow the dust to settle, before seeing improvement later in the year,” Parsons said. “So perhaps the year-end 2017 numbers end up looking a lot like 2015 and 2016, in terms of volume.”

Q&A with Philip Martin

In a questions and answers session, Waterton’s Philip Martin joined the webcast to reflect on the headlining topics. The researcher expressed chaos is accompanied by opportunity, and changes will not equally impact the industry’s participants.

“Inflation and higher interest rates are on the way, but it will play itself out in different ways, in different markets,” Martin said.

For the industry as a whole, Martin foresees more construction activity. On supply, he noted the industry must ask if existing housing meets existing and future needs.

“The older age cohort, we’re seeing more demand there,” he noted as an example. “And we would expect to see more demand from the older age cohort, going forward, especially as they’re able to sell homes, which we think will be increasingly more likely.”